[ad_1]

Justin Sullivan

Why An Exchange Is Better Than A Currency

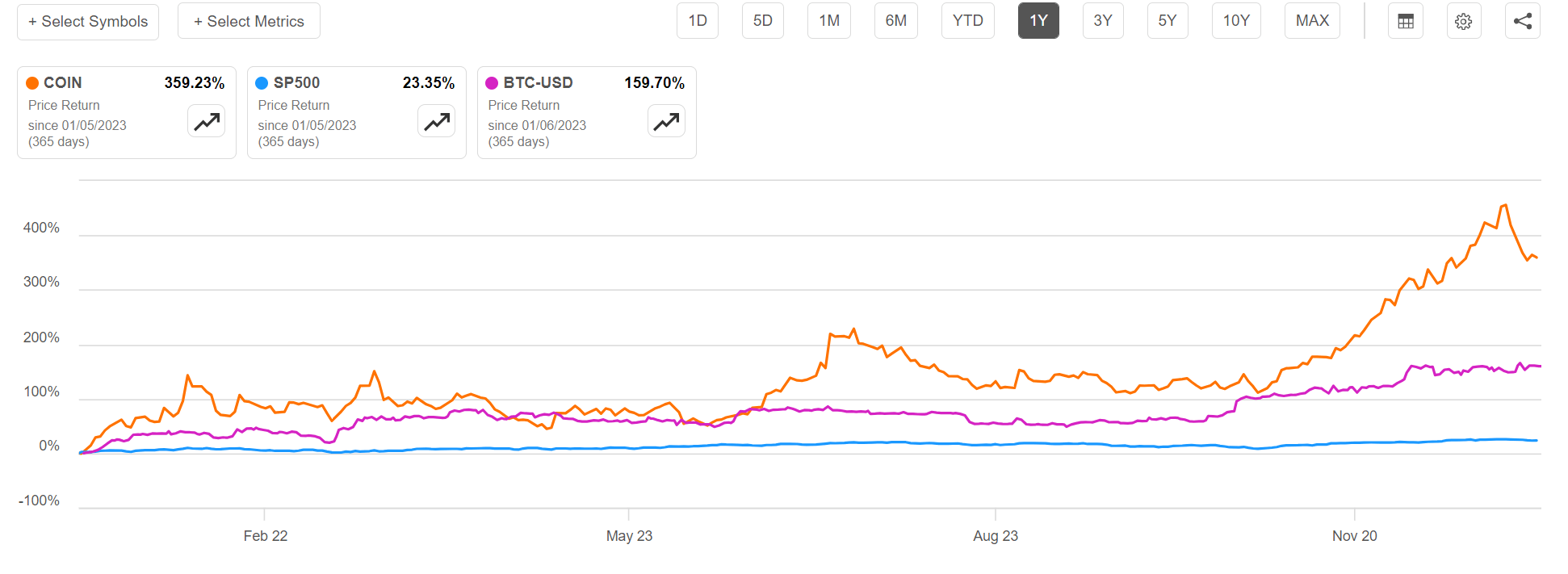

Cryptocurrencies have seen a strong bull market in 2023, with the BTC-USD trading pair returning almost 160% for the trailing twelve months, compared to a gain of only 23% for the S&P 500 (SP500). Meanwhile, assets levered to the crypto market have rallied with the currencies: In fact, Coinbase (NASDAQ:COIN) shares appreciated by more than 360% and have thus grossly outperformed the Bitcoin benchmark.

Seeking Alpha

Coinbase strong outperformance vs. Bitcoin makes sense, in my opinion: Firstly, I point out that investing in Coinbase, a cryptocurrency exchange, as opposed to Bitcoin itself, aligns with the concept of investing in productive versus non-productive assets. Specifically, as an exchange, Coinbase earns revenue through transaction fees, custodial services, and other products. Its income potential is thus linked to the growing adoption and trading volumes of various cryptocurrencies. Conversely, when you invest in Bitcoin, you’re essentially purchasing a non-productive asset. Bitcoin doesn’t generate income or dividends; its value is solely based on market demand.

As the adoption of cryptocurrencies rises, Coinbase stands to benefit from increased trading volumes across multiple cryptocurrencies, not just Bitcoin. In addition, Coinbase represents a platform rather than a uno asset. By investing in Coinbase, investors are not limited to Bitcoin but gain exposure to various cryptocurrencies available on the platform. This diversification can mitigate risk compared to holding a single cryptocurrency. On a related note, Coinbase continually expands its offerings, including staking, lending, and other financial services. This broader ecosystem might attract more traditional investors looking for exposure to the cryptocurrency market without directly holding cryptocurrencies. Lastly, Cryptocurrency prices can be highly volatile. Coinbase’s business model isn’t solely reliant on the price movement of one asset. Even if Bitcoin experiences a downturn, Coinbase could still generate revenue from other cryptocurrencies and services it offers.

Coinbase May Be Winning The Exchange War

Having established that it is better to own an exchange, rather than coins, it is noteworthy to point out that Coinbase is a frontrunner in the crypto exchange space. Coinbase is known for its user-friendly interface, security measures, and robust regulatory compliance. Its first-mover advantage and brand recognition have helped the company amass a large customer base of 73 million verified users. On that note, I am especially bullish on Coinbase’s expansion opportunity as the leading crypto exchange after key competitors FTX and Binance have stumbled. The FTX story does likely not need context; The Binance story is based on regulatory issues faced in the United States. Specifically, federalista agencies like the CFTC, FinCEN, and OFAC took legal actions against Binance due to compliance concerns. This eventually led to the resignation of CEO Changpeng Zhao and a $4.3 billion settlement agreement with authorities.

As an additional argument speaking for Coinbase, I like that the company is continually introducing new services and products, thus expanding its ecosystem. Features like staking rewards, crypto loans, NFT marketplaces, and institutional-grade services have highlighted the company’s adaptability and capacity to evolve with the fast-changing crypto landscape. Most recently, Coinbase initiated spot trading on its International Exchange and commenced operations with Project Diamond, a smart contract platform that enables institutions to create and trade tokenized assets. Additionally, Coinbase recently shared via Twitter that they had raised the leverage for perpetual futures trading on their international exchange to 10x. Previously, these products offered leverage ranging from 3x to 5x, depending on the specific products traded.

2024 Setting Up To Provide a Bullish Backdrop

Although some of the recent momentum in Crypto prices could likely be attributed to Cryptocurrency’s perceived role as a “safe haven” asset amid geopolitical tensions, the sustained surge is also underpinned by a broader global appetite for an inflation hedge (following the 2021-2022 inflation pain, many investors and households are arguably looking for a hedge). Furthermore, the anticipation of rate cuts, predicted to materialize in 2024, is supporting Crypto prices. It’s essential for investors to recognize that lower rates obséquio Crypto by decreasing the opportunity cost of holding non-yielding assets. Moreover, reduced rates can potentially depreciate currencies, heightening Crypto’s attractiveness as a hedge against inflation and currency devaluation.

Moreover, approaching 2024 there are quite a few interesting developments that may support the appeal of Crypto to households and investors, as Crypto currencies receive validation from key market participants.

- On 12/12/23, S&P introduced an assessment to evaluate stablecoins’ ability to maintain a steady value relative to their pegged fiat currencies.

- On 12/21/23, Argentina’s Minister of Foreign Relations confirmed the country’s endorsement of using cryptocurrencies as official visar in contracts.

- On 12/12/23, BlackRock adjusted its proposed spot bitcoin ETF mechanics, allowing authorized participants to create new fund shares using cash instead of cryptocurrency, enabling cash exchange for bitcoin by an intermediary to be stored by the ETF provider.

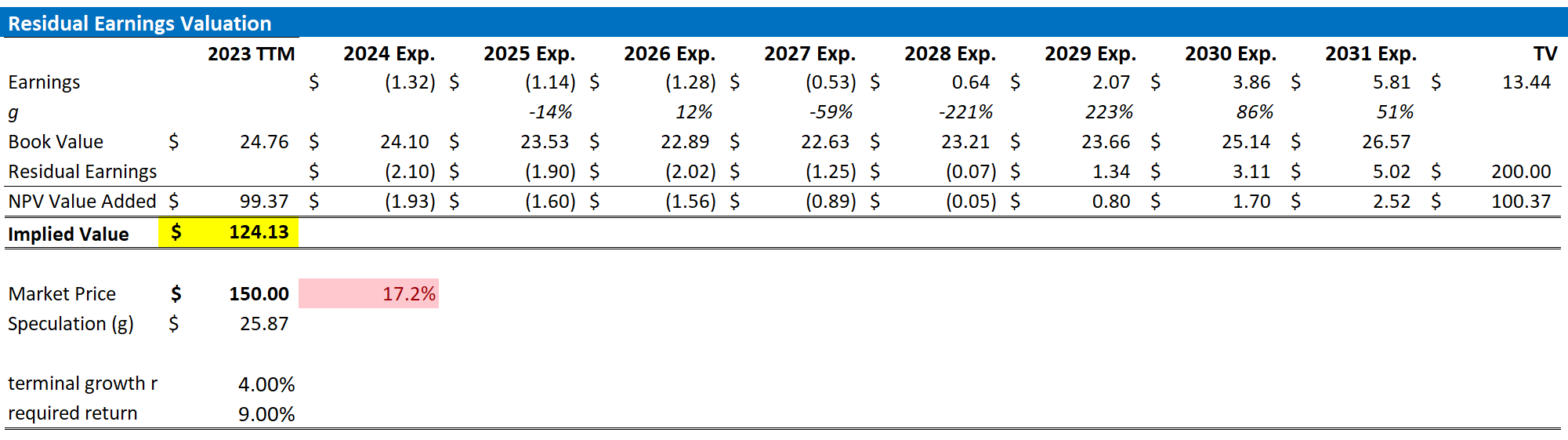

COIN Valuation: Set TP At $124/Share

Valuing a growth asset like Coinbase is difficult. Thus, I advise readers to approach my residual income model with some healthy skepticism. My model anchors on the idea that a valuation should equal a business’ discounted future earnings after capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my COIN stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on Seeking Alpha.

- To estimate the capital charge, I anchor on COIN’s cost of equity at 9%.

- For the terminal growth rate after 2025, I apply 4%, which is about 125-150 basis points above the estimated nominal global GDP growth. The growth premium should reflect the structural expansion outlook of the Crypto market with a long-dated penetration runway.

Given these assumptions, I calculate a base-case target price for COIN stock of about $124/share.

Seeking Alpha; Company Financials; Author’s Calculations

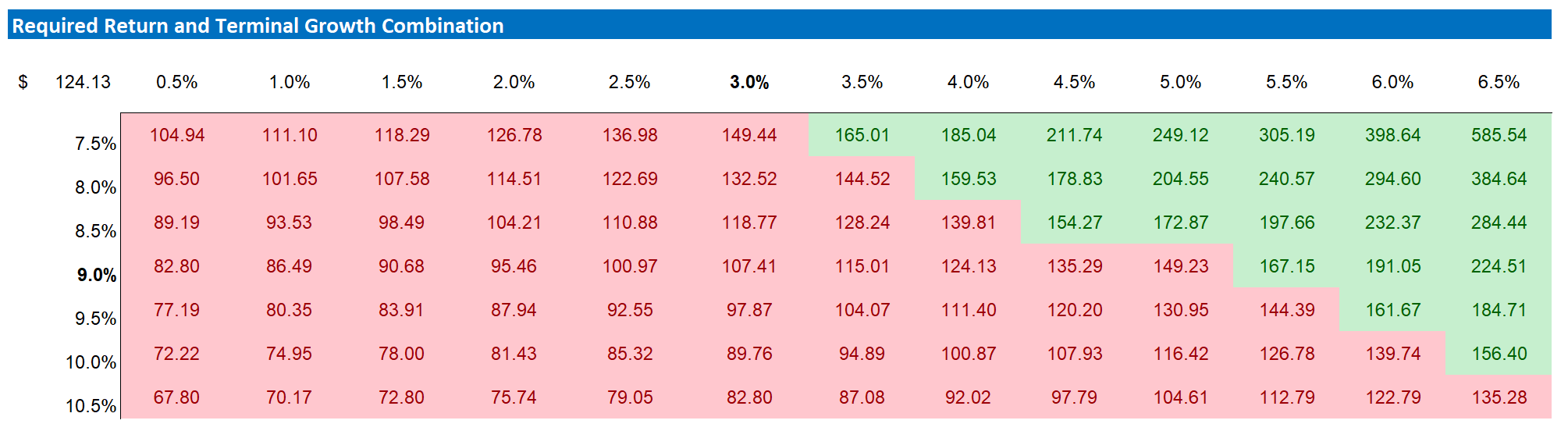

As I argued that my estimates for growth and equity charges may be conservative, I acknowledge that investors may hold varying assumptions regarding these rates. Therefore, I’ve included a sensitivity table to test different scenarios and assumptions. See below.

Seeking Alpha; Company Financials; Author’s Calculations

A Note On Risks

Investing in Coinbase presents potential risks relating to the company’s reliance on crypto asset prices and transaction volumes. Fluctuations or prolonged declines in these areas could notably impact the company’s operations. Moreover, Coinbase operates in a rapidly changing regulatory environment within the expanding crypto economy. Compliance with evolving financial laws and regulations is crucial, and failure to do so could lead to severe consequences, including fines, license revocation, service restrictions, and damage to its reputation (see FTX and Binance).

Investor Takeaway

Broadly speaking, I cautiously anticipate the ongoing evolution and strengthening of the do dedo asset ecosystem (crypt industry) to gradually influence nearly every aspect of the economy.

This influence could encompass various sectors, including the tokenization of real-world assets, modernizing financial systems through payments, remittance, staking, yield earning, and more. In that context, I foresee Coinbase having the potential to emerge as one of the major winners in this rapidly expanding and evolving crypto industry.

While I am bullish on Coinbase’s commercial momentum, I point out that shares are trading cheap, with COIN stock being traded at 12x EBIT/ EV (FWD). As a function of accounting for both business quality and valuation, I assign a “Hold” rating.

[ad_2]